Current Market Valuations

In conjunction with our review of private company transaction we have prepared a detailed paper on UK PLC’s.

UK PLC Software valuations remained robust in Q320 despite the additional lock down and implementation of tier based restrictions. Systems software and application software led the pack followed by application software and e-commerce.

Note: Both are Enterprise Value Multiples (Left is Revenue Multiple, Right is EBITDA multiple)

Notable software companies include:

• Blue Prism Group: 9.3 Rev x, 1Y Growth 77.6%, 3Y CAGR 105%

• Deep Matter Group Plc 7.3 Rev x, 1Y growth 603%

Blue Prism Group is engaged in business process automation, it enables blue chip companies to create a digital workforce powered by the Company’s software robots that are trained to automate back-office clerical tasks.

Deep Matter Group provides retro synthesis and reproducibility in chemistry. It develops software to deliver applications resulting in new optimisation chemicals, materials and scientific and formulations in commercially significant areas, such as pharmaceutical research and fine chemicals.

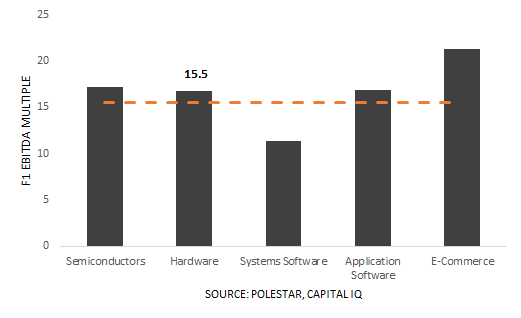

One year from now, sell-side analysts are pricing e-commerce companies 1.3 EBITDA turns higher and for system software EBITDA multiples to recede significantly.

Forward Software Multiples

COVID-19 Impact

• Shift towards home working has catalysed the demand for collaboration and enterprise software.

Note: Both are Enterprise Value Multiples (Left is Revenue Multiple, Right is EBITDA multiple)

Opinion

• SaaS stocks should not be seen as contingent on work-from-home. Business model means services are paid through operating budget, which is multiples larger than CapEx budgets. Additionally, they are often targeted at cutting down labour intensive tasks, solidifying their intrinsic value.

Revenue Multiples vs Growth Rates

• Faster growing sectors command higher multiples.

• Systems software companies have grown by 32.3% over the last year and by 44% over the past three.

• Hardware businesses are being priced around 1-3 Rev x and growth rates around 15%. Note that hardware valuations are also suppressed by higher cost of customer acquisition, lower degree of recurring revenue and more pronounced capital requirements.

EBITDA Multiples vs EBITDA Margins

• Note that since these are public companies, they are relatively mature compared to all UK software businesses. Although the correlation between margin and multiples visually look to be pronounced, it isn’t a straight forward equation. As such, when looking at smaller private companies, the impact of EBITDA margin on valuation tends to be less noticeable and more influenced by revenue quantum and growth and other qualitative factors.

• Note that since these are public companies, they are relatively mature compared to all UK software businesses. Although the correlation between margin and multiples visually look to be pronounced, it isn’t a straight forward equation. As such, when looking at smaller private companies, the impact of EBITDA margin on valuation tends to be less noticeable and more influenced by revenue quantum and growth and other qualitative factors.

• Application/Systems software companies command the highest average EBITDA multiples and on average achieve greater than 13% EBITDA margins.

• Despite having slightly weak margins compared to hardware, e-commerce companies are still commanding higher EBITDA multiples (c. 20x).

You can find the full document and appendices here:

http://polestarcf.com/wp-content/uploads/2020/11/SaaS-Q320-Public-Company-Snapshot.pptx

SaaS stocks should not be seen as contingent on work-from-home. Business model means services are paid through operating budget, which is multiples larger than CapEx budgets. Additionally, they are often targeted at cutting down labour intensive tasks, solidifying their intrinsic value.